Tips for Enhancing Your Child’s Financial Literacy

Understanding Basic Financial Concepts

Developing financial awareness begins with grasping fundamental concepts like budgeting, saving, investing, and debt management. Understanding how income is generated, how expenses are categorized, and the importance of setting financial goals are crucial first steps. Without this foundational knowledge, building a strong financial future becomes significantly more challenging. Learning about different types of accounts, such as checking and savings, and the benefits of each is also important for effectively managing your money.

This initial phase is about laying the groundwork for informed decision-making. It involves learning about interest rates, compound interest, and how these factors affect your finances over time. A strong understanding of these concepts will be invaluable as you progress to more complex financial strategies.

Creating a Realistic Budget

A budget is a roadmap for your money, outlining where your income goes and how you allocate it. Creating a realistic budget involves tracking all your income sources, recording every expense, no matter how small, and identifying areas where you can cut costs. This process helps you understand your financial situation and identify areas for improvement. A well-structured budget provides a framework for achieving financial goals, and is essential in determining areas for saving, investing, or paying down debt.

Saving for the Future: Importance of Emergency Funds

Establishing an emergency fund is one of the most important steps in building financial security. An emergency fund provides a safety net for unexpected expenses, such as car repairs, medical bills, or job loss. Having this cushion allows you to avoid taking on high-interest debt when unexpected financial challenges arise. This will allow you to take control of your financial decisions rather than having to react out of panic or desperation.

Building an emergency fund isn't just about saving a lump sum; it's about establishing a consistent savings habit. Regular contributions, even small ones, make a significant difference over time, ensuring you have a safety net when needed.

Managing Debt Effectively

Debt can be a significant obstacle to achieving financial stability. Understanding different types of debt, such as credit card debt, student loans, and mortgages, is vital. Developing a strategy for managing and paying down debt is crucial for avoiding high-interest charges and the associated stress. Prioritizing high-interest debts and making consistent payments toward them is key to managing debt effectively.

Investing for the Long Term: Simple Strategies

Investing early in your life, even with small amounts, can have a profound impact on your financial future. Understanding basic investment options like savings accounts, certificates of deposit, and stocks is a helpful starting point. Learning about diversification and risk tolerance is essential for making informed investment choices. Exploring different investment options and understanding how different options can affect your future is important for decision-making in the long term.

Utilizing Technology for Financial Management

Technology offers numerous tools to assist in managing finances more effectively. Online budgeting apps, investment platforms, and financial tracking software provide a structured approach to saving and managing money. Using these tools can empower you to monitor your progress and make adjustments to your financial plan as needed. Utilizing these tools can help you stay on track and improve your financial literacy through helpful insights and information.

Seeking Professional Guidance

Don't hesitate to seek professional financial advice from a qualified advisor. They can provide personalized guidance and strategies tailored to your specific circumstances and goals. Experienced financial advisors can provide valuable insight and support in navigating complex financial matters. They can help you design a comprehensive financial plan and offer advice based on your unique needs and circumstances, which is a valuable tool for securing financial stability.

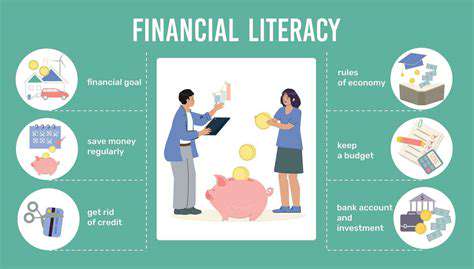

Budgeting Basics: Managing Money Effectively

Understanding Your Income and Expenses

A crucial first step in budgeting is understanding your income and expenses. This involves meticulously tracking all sources of income, including salary, side hustles, or any other financial inflows. Accurate recording is essential to understand where your money is coming from and to get a clear picture of your financial resources. Conversely, identifying and categorizing all expenses, both fixed (rent, mortgage, utilities) and variable (groceries, entertainment, transportation), is equally important. This comprehensive overview allows for realistic financial planning and helps you identify areas where you might be overspending.

Detailed expense tracking, whether through budgeting apps or a simple spreadsheet, reveals patterns in spending habits. By identifying recurring expenses and understanding their amounts, you can effectively plan for them and make informed decisions about savings, investments, or adjustments to your spending habits.

Creating a Realistic Budget

Developing a budget that accurately reflects your financial situation is paramount. Avoid creating unrealistic goals; a budget that's too restrictive can lead to frustration and abandonment. Instead, strive for a balance that allows for necessary expenses while also incorporating savings and potential financial goals. Analyze your income and expenses to establish a realistic spending plan. This includes acknowledging your financial commitments and incorporating them into your budget.

Setting Financial Goals

Budgeting isn't just about tracking expenses; it's about achieving financial goals. Whether it's saving for a down payment on a house, funding your child's education, or simply building an emergency fund, setting clear financial objectives helps provide direction and motivation. Defining these goals will shape your budgeting strategy, helping you prioritize saving and making informed financial decisions. Understanding and prioritizing your financial objectives is vital for successful budgeting.

Prioritizing Savings and Investments

Allocating a portion of your budget to savings and investments is a critical component of effective financial management. This involves setting aside money for unexpected expenses, long-term goals, or building a retirement fund. Determining how much you can realistically save each month is a crucial part of this process. Understanding the different investment options available, and their potential risks and rewards is vital to making informed decisions.

Monitoring and Adjusting Your Budget

A budget isn't a static document; it's a living tool that needs regular monitoring and adjustment. Periodically reviewing your progress against your budget helps you identify areas where you're exceeding or falling short of your planned expenses. Regularly evaluating spending patterns allows for course correction and adjustments in spending habits. This dynamic approach ensures that your budget remains relevant to your evolving financial situation.

Read more about Tips for Enhancing Your Child’s Financial Literacy

Hot Recommendations

- Efficient Study Habits for Middle Schoolers

- How to Foster Cooperation Between Co Parents

- Best Education Techniques for Children with Autism

- Supporting Special Needs Kids: Strategies for Education and Companionship

- How Can I Improve Early Childhood Learning at Home?

- How to Navigate Different Parenting Styles Together

- How to Create Consistency with Positive Discipline Techniques

- Step by Step Guide to Positive Behavior Management

- Tips for Encouraging Social Skills in Children with Autism

- How to Support Special Needs Children at Home