Best Free Resources for Teaching Kids Money Management

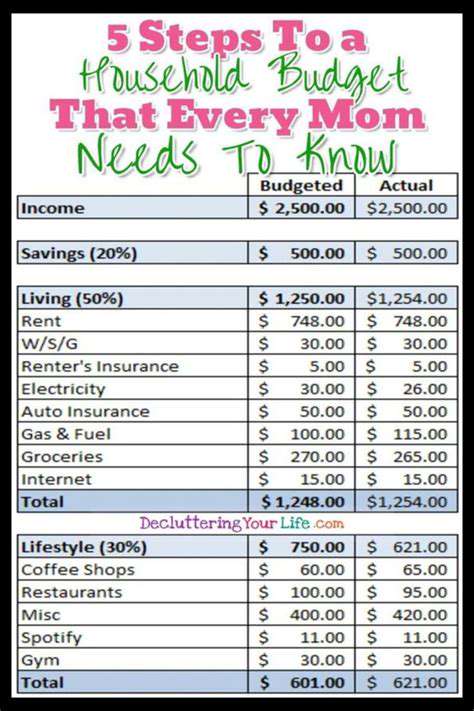

Creating a Family Budget (with Kid-Friendly Participation)

Understanding Family Needs

Creating a family budget is more than just crunching numbers; it's about understanding your family's unique needs and priorities. This involves considering everyone's individual requirements, from basic necessities like food and shelter to extracurricular activities and personal expenses. Careful consideration of each family member's needs will help ensure that everyone's financial needs are met, and that the budget is sustainable and realistic for the long term.

It's crucial to distinguish between needs and wants. While both are important, focusing on needs first will allow for a more stable financial foundation for the entire family.

Tracking Income and Expenses

A vital first step in creating a family budget is meticulously tracking both income and expenses. This involves recording every source of income, from salaries to side hustles, and meticulously documenting each expense, regardless of how small. This detailed record will provide a clear picture of your financial inflows and outflows, allowing you to identify areas where you can save money or adjust spending habits. Understanding where your money is going is essential for effective budget management.

Setting Realistic Financial Goals

Defining clear and achievable financial goals is crucial for motivating your family and ensuring the budget aligns with your aspirations. Whether it's saving for a down payment on a house, funding your children's education, or simply building an emergency fund, establishing these goals provides a roadmap for your financial journey. Setting realistic goals will help you feel more in control of your finances and less overwhelmed. Make sure the goals are specific, measurable, achievable, relevant, and time-bound (SMART goals) for better results.

Allocating Funds to Different Categories

Once you have a thorough understanding of your income and expenses, the next step is to allocate funds to different categories within your budget. This involves creating specific budget lines for essentials like housing, food, transportation, healthcare, and childcare. It is also important to allocate funds for entertainment, savings, and debt repayment. Careful allocation will ensure that all necessary expenses are covered and that you're setting aside money for future needs and financial security.

Reviewing and Adjusting the Budget

A family budget isn't a static document; it needs regular review and adjustment to reflect changing circumstances. Life throws curveballs, and unexpected expenses or income fluctuations can impact your budget. Regular review and adjustments will keep your budget aligned with your family's evolving needs and goals. Reviewing your budget monthly or quarterly will help you stay on track, identify areas for improvement, and make necessary adjustments to ensure its effectiveness in supporting your family's financial well-being.

Storytelling and Books on Financial Concepts

Using Stories to Explain Complex Ideas

Storytelling is a powerful tool for making abstract financial concepts more relatable and engaging for children. A well-crafted story can illustrate the importance of saving, the risks of spending impulsively, and the rewards of investing. Instead of simply stating that saving money is good, a story can demonstrate how saving can lead to achieving a goal, like buying a toy or a trip. This approach makes the concept tangible and memorable, fostering a deeper understanding of financial principles.

Illustrating the concept of delayed gratification with a story about a child who chooses to save for a special item instead of buying candy every day can make this important concept more impactful. This method helps children visualize the value of waiting for something they want and the benefits of saving.

Books Focusing on Saving and Spending

Numerous children's books explore saving and spending habits. These books often use relatable characters and engaging plots to teach children about the importance of budgeting, saving for future needs, and making wise financial choices. These books can be a valuable addition to educational resources, providing children with practical examples and illustrations to reinforce their understanding.

Finding books that align with a child's age and comprehension level is crucial. Age-appropriate stories will resonate more deeply and help children grasp the concepts being presented. Looking for books with engaging illustrations and simple language can make the learning experience more enjoyable.

Exploring the Concept of Investing

While the concept of investing might seem complex for young children, age-appropriate books can introduce the idea of earning returns on money. These books can use simple analogies to illustrate how savings grow over time. This can include stories about seeds growing into plants or money earning interest in a savings account, making the abstract concept more accessible.

Stories about entrepreneurship and starting a business can introduce the concept of risk and reward in an enjoyable way. These stories can help children understand that some decisions will yield more money than others, while also showing the dedication and hard work required for any business venture. This can help foster a basic understanding of financial risks and rewards.

Understanding Budgeting and Financial Responsibility

Books that focus on budgeting and financial responsibility can teach children the importance of managing their money effectively. They can emphasize the need for creating a budget, prioritizing needs over wants, and saving for future goals. These books can offer practical tips and tricks for kids to manage their allowance or earnings.

By using relatable scenarios, these books can help children understand the importance of setting financial goals, tracking expenses, and making responsible choices with their money. They can use stories about making choices between buying things they want or saving for something more important, reinforcing the importance of budgeting.

Books Featuring Money Management Through Games

Interactive books, or books that incorporate games, are excellent tools for making financial concepts more engaging. Games can encourage children to apply the lessons they've learned through storytelling and examples. These games can be simple activities, like matching different spending categories or calculating the cost of different items. A game-based approach makes learning fun and encourages active participation.

The Role of Books in Shaping Financial Habits

Children's books on financial concepts play a significant role in shaping a child's financial habits and attitudes towards money. By introducing children to these concepts early on, parents and educators can help them develop a strong foundation for future financial literacy. These books can instill the importance of saving, budgeting, investing, and making responsible financial decisions.

Using books as a starting point for discussions about money can empower children to ask questions and explore their own ideas about finances. This can be a great way to start conversations with kids and encourage them to think critically about their own money management strategies.

Read more about Best Free Resources for Teaching Kids Money Management

Hot Recommendations

- Efficient Study Habits for Middle Schoolers

- How to Foster Cooperation Between Co Parents

- Best Education Techniques for Children with Autism

- Supporting Special Needs Kids: Strategies for Education and Companionship

- How Can I Improve Early Childhood Learning at Home?

- How to Navigate Different Parenting Styles Together

- How to Create Consistency with Positive Discipline Techniques

- Step by Step Guide to Positive Behavior Management

- Tips for Encouraging Social Skills in Children with Autism

- How to Support Special Needs Children at Home